Car loan payments in 2026 have reached record highs, leaving many Americans stunned at dealership desks. Rising vehicle prices, elevated interest rates, longer loan terms, and tighter lending standards have quietly transformed auto financing. This in-depth guide reveals why car payments are so expensive, who is most affected, and what buyers can do to avoid long-term financial damage in today’s auto market.

Why Car Loan Payments in 2026 Are Shocking Americans Nationwide

Across the United States, something remarkable—and deeply unsettling—is happening in car dealerships.

Buyers walk in with realistic expectations, confident they’ve done their research, only to freeze when the salesperson slides the payment sheet across the desk. The number staring back at them doesn’t feel like a car payment anymore. It feels like rent.

What’s especially jarring is that these reactions are coming from people who are financially responsible. They have decent credit. Stable income. Reasonable expectations. Yet the monthly payments they’re being quoted in 2026 feel disconnected from reality.

This isn’t just inflation anxiety or social media exaggeration. It’s a real structural change in how cars are priced, financed, and sold in America.

How High Are Car Payments Really in 2026?

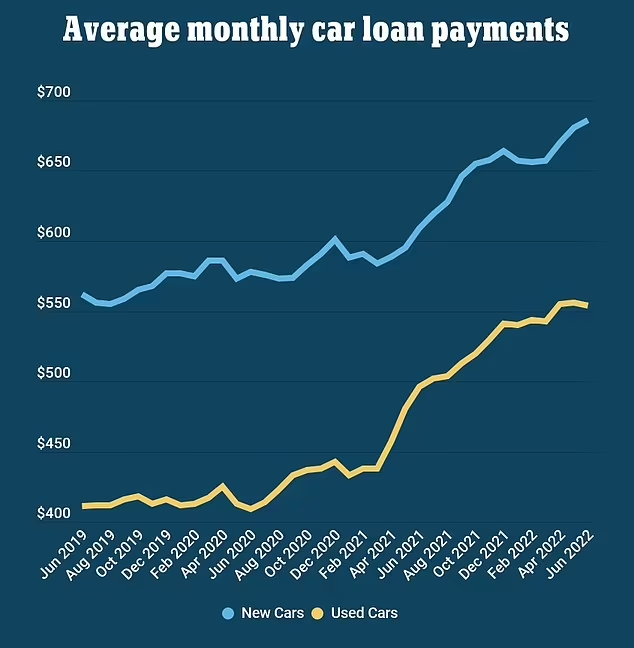

For decades, Americans grew accustomed to a certain range when it came to car payments. Around $300 felt manageable. $400 felt like a stretch. Anything above $500 was considered luxury territory.

That mental framework no longer applies.

In 2026:

- Many new-car buyers are paying $700 to $850 per month

- Used-car payments frequently exceed $500

- Loan terms are stretching six to seven years, sometimes longer

- Interest costs alone can rival the price of a used car from a decade ago

A real-life example

Brandon, a 38-year-old sales manager in Nevada, recently traded in his aging sedan. He didn’t splurge. He chose a practical midsize SUV to accommodate his growing family.

Sticker price: just under $43,000

Down payment: $5,000

Credit score: good

Loan term: 72 months

Monthly payment: $768

Brandon earns a solid income, but the payment still made him uncomfortable. Ten years earlier, a similar purchase would have cost hundreds less per month.

Why Car Loan Payments Have Skyrocketed in 2026

1. Vehicle Prices Never Truly Fell Back to “Normal”

While supply chain issues eased compared to earlier years, vehicle prices never returned to pre-crisis levels. Instead, manufacturers quietly restructured their offerings.

Automakers:

- Reduced production of low-margin, entry-level vehicles

- Focused on higher-priced trims

- Bundled advanced technology into standard models

- Raised base prices permanently rather than temporarily

As a result, the “cheap new car” has nearly vanished from the US market.

For many buyers, there is no longer a meaningful difference between a base model and a mid-tier model in terms of monthly payment—both are expensive.

2. Interest Rates Reshaped Auto Financing Overnight

Interest rates are one of the most powerful drivers of monthly payments, yet they are often underestimated by buyers.

Even small increases in rates have massive effects when applied over long loan terms.

Consider this scenario

A $45,000 auto loan:

- At 3% interest produces a manageable payment

- At 7–9% interest adds hundreds per month

- Over 72–84 months, total interest can exceed $15,000–$20,000

Many Americans focus on vehicle price and ignore how dramatically interest changes the final cost.

In 2026, interest is no longer a footnote—it’s a central factor.

3. Loan Terms Are Longer Than Ever Before

To make payments appear affordable, lenders have increasingly pushed extended loan terms.

Common loan lengths now include:

- 72 months

- 84 months

- Occasionally even longer structures

While these loans reduce the monthly number slightly, they come with serious consequences.

Long-term effects:

- Drivers remain upside-down on loans for years

- Trade-ins become difficult

- Interest costs balloon

- Financial flexibility disappears

Many Americans now owe more on their cars than they’re worth for most of the loan’s lifespan.

4. Used Cars Are No Longer the Safe Escape Route

Buying used used to be the financially smart alternative. In 2026, that advantage has narrowed dramatically.

Used vehicle prices remain high due to:

- Fewer trade-ins from earlier years

- Longer ownership cycles

- Heavy demand from buyers priced out of new cars

On top of that, interest rates on used car loans are often higher than those for new vehicles, erasing much of the savings.

Who Is Being Hit the Hardest by High Car Payments?

Middle-Income Households

Families earning between $60,000 and $100,000 are under the most pressure. They earn too much to qualify for assistance but not enough to comfortably absorb $700+ monthly payments.

First-Time Buyers

Younger Americans with limited credit history often face higher rates, making even modest cars expensive.

Rural and Suburban Drivers

In areas with limited public transportation, car ownership isn’t optional. High payments hit these communities especially hard.

The Emotional Weight of Modern Car Payments

Car payments in 2026 don’t just strain budgets—they affect mental health and life decisions.

Many buyers report:

- Immediate regret after purchase

- Anxiety tied to job security

- Reduced savings

- Delayed milestones like homeownership or family planning

A real-life story

Angela, a healthcare worker in Missouri, replaced her aging vehicle after repeated breakdowns. Within months, she found herself reshaping her entire budget around the car payment.

She wasn’t unhappy with the car—but the financial pressure was constant.

The car became less a convenience and more a source of stress.

Why “Just Buy Cheaper” No Longer Works

Traditional advice often fails in today’s market.

Problems buyers face include:

- Limited availability of low-cost models

- Long waits for base trims

- Mandatory technology packages

- Financing costs outweighing vehicle choice

In many cases, choosing a “cheaper” vehicle only lowers the payment slightly—while sacrificing comfort or reliability.

The Hidden Costs That Make Car Ownership Even More Expensive

The loan payment is only part of the story.

Drivers in 2026 also face:

- Higher insurance premiums

- Rising repair and maintenance costs

- Expensive replacement parts

- Subscription-based vehicle features

When combined, the true monthly cost of owning a car often far exceeds the loan payment alone.

How Americans Are Coping With High Car Payments

Some buyers are adapting cautiously:

- Keeping cars longer than ever

- Sharing vehicles within households

- Choosing certified pre-owned cars

- Delaying purchases when possible

Others are stretching themselves dangerously thin, leaving little margin for emergencies.

What Smart Car Buyers Are Doing Differently in 2026

Despite the tough market, informed buyers are making better decisions.

They focus on:

- Larger down payments

- Shorter loan terms

- Pre-approved financing

- Negotiating total cost, not monthly payment

- Avoiding add-ons rolled into loans

- Understanding the full interest impact

These strategies don’t eliminate high costs—but they reduce long-term damage.

How Long Will High Car Payments Last?

Most industry observers agree:

- Vehicle prices may stabilize, not collapse

- Interest rates may ease slowly

- Long loan terms are here to stay

High car payments are not a temporary anomaly. They are becoming the new normal.

Why This Matters for American Financial Health

Car loans affect far more than transportation.

They influence:

- Credit scores

- Debt-to-income ratios

- Mortgage eligibility

- Emergency savings

- Retirement contributions

When car payments grow too large, they quietly undermine long-term financial stability.

Frequently Asked Questions (Trending in the US)

1. Why are car payments so high in 2026?

Because vehicle prices, interest rates, and loan terms have all increased simultaneously.

2. What is the average car payment right now?

Many new-car buyers pay over $700 per month; used-car payments often exceed $500.

3. Will car prices go down soon?

Prices may stabilize, but major drops are unlikely in the near future.

4. Is leasing better than buying in 2026?

Leasing may lower short-term payments but often costs more long-term.

5. Why are used car loans so expensive?

High demand and higher interest rates on used vehicles drive up payments.

6. How long should a car loan be?

Shorter terms reduce interest but increase monthly payments. Balance is key.

7. Can high car payments hurt my credit?

Yes. They increase debt ratios and raise the risk of missed payments.

8. Should I wait to buy a car?

If you can, waiting may help—but not everyone has that option.

9. How much car payment is too much?

Experts often suggest keeping total car costs under 15% of take-home pay.

10. What is the biggest mistake buyers make today?

Focusing only on monthly payment instead of total loan cost.

Final Takeaway: This Is More Than Sticker Shock

Car loan payments in 2026 are high not because Americans are irresponsible—but because the auto market has fundamentally changed.

Understanding these shifts is essential for making smarter decisions and avoiding years of financial stress.

The car you drive should support your life—not control it.