I committed to a 30-day no-spend challenge expecting savings and financial clarity. Instead, I faced emotional discomfort, social friction, and some hard truths about modern spending habits. This in-depth, real-life breakdown reveals what actually happens during a no-spend month, why the results can feel brutal, and whether this challenge truly helps—or hurts—your finances.

Introduction: Why the No-Spend Challenge Sounded Like the Perfect Fix

The no-spend challenge has become one of the most talked-about personal finance experiments online. Scroll through social media and you’ll see confident creators claiming they saved hundreds—sometimes thousands—of dollars simply by not spending money for a month. The concept is simple, bold, and appealing: stop unnecessary spending, reset your habits, and regain control of your finances.

At the time I started, my finances weren’t a disaster. I paid my bills on time. I had a steady income. But I constantly felt behind. My savings barely grew, unexpected expenses threw off my budget, and every month ended with the same quiet frustration: Why does my money disappear so fast?

Like many Americans, I wasn’t overspending recklessly—I was just stuck in a system of automatic expenses, convenience purchases, and emotional spending. The no-spend challenge promised clarity and discipline. So I committed to 30 days, fully expecting discomfort but also hoping for a breakthrough.

What I didn’t expect was how emotionally demanding it would be—and how brutally honest it would force me to become about my relationship with money.

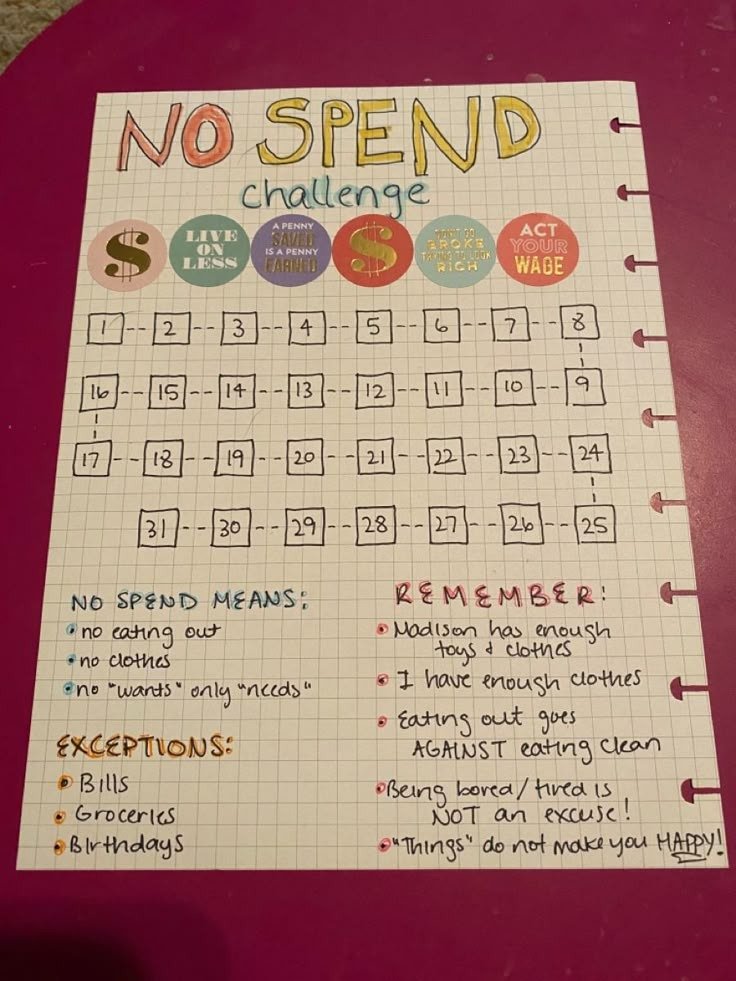

What Is a No-Spend Challenge, Exactly?

Despite its popularity, the no-spend challenge is often misunderstood. It’s not about spending zero dollars. It’s about spending only on true necessities for a defined period of time.

In most versions, the challenge allows fixed, unavoidable expenses while pausing discretionary spending.

Common No-Spend Rules

Most people follow guidelines like these:

- Allowed: rent or mortgage, utilities, groceries, transportation, medical needs

- Not allowed: dining out, entertainment, shopping, online orders, impulse buys

- Gray areas: gifts, social events, convenience spending

The real purpose isn’t deprivation—it’s awareness. By removing optional spending, you’re forced to see how much of your money normally goes out without conscious thought.

Days 1–5: Motivation, Control, and Overconfidence

The first few days were surprisingly easy. I felt energized and disciplined. Cooking at home felt productive. Turning down purchases felt empowering. Every time I resisted spending, I felt like I was winning.

This early phase is common. Psychologists call it the novelty effect—new challenges trigger motivation and optimism. I even started mentally judging past purchases that suddenly seemed unnecessary.

At this stage, the no-spend challenge feels like a revelation. You think, Why didn’t I do this sooner?

That confidence, however, doesn’t last.

Days 6–10: When Spending Turns Out to Be Everywhere

By the end of the first week, the cracks appeared. I realized how deeply spending is embedded in daily life.

Grabbing coffee with a friend. Ordering food after a long day. Paying for convenience when exhausted. None of these felt extravagant—but they were suddenly off-limits.

Unexpected Frictions I Didn’t Anticipate

- Social interactions often revolve around spending

- Convenience purchases reduce mental fatigue

- Boredom usually leads to small purchases

Without spending as an outlet, I had to sit with discomfort instead of bypassing it. That was harder than I expected.

Why the No-Spend Challenge Feels So Emotionally Intense

Modern spending isn’t just transactional—it’s emotional. We spend to reward ourselves, connect with others, reduce stress, and save time. Removing spending removes those coping mechanisms.

During the challenge, I noticed:

- Increased irritation when plans changed

- Frustration when convenience wasn’t available

- Emotional resistance to saying “no” socially

This discomfort isn’t a failure—it’s the point. The challenge exposes how often money is used to regulate emotions rather than meet actual needs.

Days 11–15: The Brutal Mid-Challenge Reality Check

The halfway point was the hardest emotionally.

I expected noticeable savings by now. Instead, my bank balance looked only slightly better. Fixed costs—rent, utilities, insurance—still consumed most of my income.

This led to a difficult realization: my financial stress wasn’t caused by small purchases alone.

The no-spend challenge didn’t fix structural issues like housing costs or rising insurance premiums. It highlighted them.

That realization felt discouraging at first. If cutting “fun spending” barely moved the needle, what actually would?

What the No-Spend Challenge Really Reveals About Your Finances

This is where the challenge becomes valuable—not as a money-saving hack, but as a financial diagnostic tool.

Hard Truths That Became Clear

- Fixed expenses dominate most budgets

- Discretionary spending isn’t always the core problem

- Emotional spending serves real psychological needs

- Convenience purchases often compensate for burnout

These insights were uncomfortable but powerful. They reframed my financial struggles from personal failure to systemic pressure.

Days 16–20: Subtle Wins and Unexpected Calm

Something shifted during the third week. Without spending as my default solution, I adapted.

I cooked more creatively. I walked instead of driving. I stopped browsing shopping apps out of habit. My days felt slower, quieter, and oddly more intentional.

Unexpected Benefits I Noticed

- Clearer awareness of needs vs. wants

- Reduced impulse spending after the challenge

- Less financial guilt

- Improved decision-making around money

These benefits didn’t show up as dramatic savings—but they changed my mindset.

Days 21–25: Social Pressure Becomes the Hardest Part

The most difficult part of the challenge wasn’t personal—it was social.

Friends didn’t mean harm, but phrases like “It’s just one meal” or “You’re being too strict” added pressure. Spending is a social norm, and opting out can feel isolating.

Money isn’t just personal—it’s relational. The challenge made that painfully clear.

Days 26–30: Relief, Reflection, and Realism

By the final days, I was ready for the challenge to end—not because it was unbearable, but because it wasn’t sustainable long-term.

I had saved some money, but not life-changing amounts. What I gained instead was clarity: about my habits, my triggers, and the limits of extreme restriction.

How Much Money Did I Actually Save?

This is the question everyone asks—and the answer isn’t glamorous.

The savings came mainly from:

- Eating out

- Impulse purchases

- Convenience spending

But fixed costs still dominated my budget. The challenge helped—but it didn’t transform my finances overnight.

That’s an important truth often left out of viral success stories.

Why the No-Spend Challenge Doesn’t Work for Everyone

For many Americans, the biggest financial pressures aren’t discretionary spending—they’re structural.

If most of your income goes toward:

- Housing

- Medical expenses

- Childcare

- Debt interest

Then a no-spend month can feel punishing without providing proportional relief.

What the No-Spend Challenge Is Actually Good For

Used correctly, the challenge has real value.

It Works Best As:

- A short-term awareness reset

- A habit-interruption experiment

- A spending audit without spreadsheets

It Is Not:

- A long-term financial solution

- A substitute for budgeting

- A fix for low income or high fixed costs

A More Sustainable Alternative to a Full No-Spend Month

For most people, moderation works better than extremes.

Smarter, Sustainable Options

- No-spend weekends

- Category-specific freezes (dining, shopping)

- 7-day resets each month

- 48-hour waiting periods before purchases

These approaches deliver insight without burnout.

Final Lessons From a Brutal Financial Experiment

The no-spend challenge didn’t make me rich. But it made me honest.

I learned that:

- Conscious spending beats zero spending

- Flexibility matters more than rules

- Money habits are emotional, not just logical

- Awareness is more powerful than restriction

Sometimes the most valuable financial result isn’t saving more money—it’s finally understanding how and why you spend.

Frequently Asked Questions (10 Trending FAQs)

1. What is a no-spend challenge?

A defined period where you only spend on essentials and pause discretionary purchases.

2. Does a no-spend challenge really save money?

It can, but savings vary depending on fixed expenses.

3. Is a 30-day no-spend challenge realistic?

For many people, it’s emotionally difficult and unsustainable long-term.

4. What expenses are usually allowed?

Housing, utilities, groceries, transportation, and medical costs.

5. Why does the no-spend challenge feel so hard?

Because spending is tied to emotion, convenience, and social connection.

6. Can a no-spend challenge help with debt?

It can support awareness but won’t replace a debt-reduction strategy.

7. Is it better than budgeting?

No. It works best as a supplement to budgeting, not a replacement.

8. What’s the biggest benefit of trying it?

Increased awareness of spending habits and triggers.

9. Who should avoid a no-spend challenge?

Those with extremely tight budgets or high unavoidable expenses.

10. What’s a better alternative?

Shorter no-spend periods or category-specific spending pauses.

Final Verdict: Brutal, Honest, and Eye-Opening

The no-spend challenge wasn’t a miracle cure. It didn’t eliminate financial stress or solve systemic issues. But it stripped away illusions—and that alone was powerful.

If you approach it as a learning experience rather than a punishment, the challenge can change how you see money long after the 30 days end.